RMD Rules - Retirement Account Distributions After Age 70½

If you have assets in a qualified retirement plan, such as a company-sponsored 401(k) plan or a traditional individual retirement account (IRA), you'll want to be aware of several rules that may apply to you when you take a distribution.

Required Minimum Distributions During Your Lifetime

Many people begin withdrawing funds from qualified retirement accounts soon after they retire in order to provide annual retirement income. These withdrawals are discretionary in terms of timing and amount until the account holder reaches age 70½. After that, failure to withdraw the required minimum amount annually may result in substantial tax penalties. Thus, it may be prudent to familiarize yourself with the minimum distribution requirements.

For traditional IRAs, individuals must generally begin taking required minimum distributions no later than April 1 following the year in which they turn 70½ and by December 31 every year thereafter. The same generally holds true for 401(k)s and other qualified retirement plans. (Note that some plans may require plan participants to remove retirement assets at an earlier age.) However, required minimum distributions from a 401(k) may be delayed until retirement if the plan participant continues to be employed by the plan sponsor beyond age 70½ and does not own more than 5% of the company.

In accordance with IRS regulations, minimum distributions are determined using one standard table based on the IRA owner's/plan participant's age and his or her account balance. Thus, required minimum distributions generally are no longer tied to a named beneficiary. There is one exception, however: IRA owners/plan participants who have a spousal beneficiary who is more than 10 years younger can base required minimum distributions on the joint life expectancy of the IRA owner/plan participant and spousal beneficiary.

These minimum required distribution rules do not apply to Roth IRAs. Thus, during your lifetime, you are not required to receive distributions from your Roth IRA.

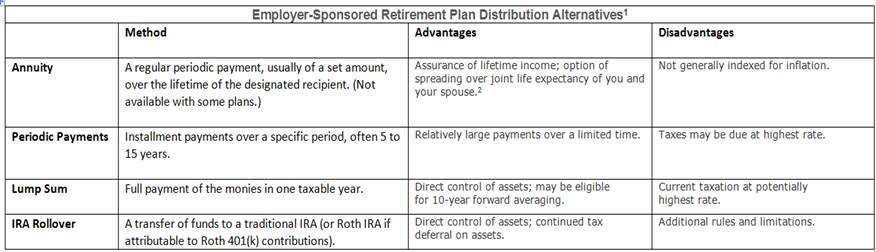

Additional Considerations for Employer-Sponsored Plans

The table below is general in nature and not a complete discussion of the options, advantages, and disadvantages of various distribution options. For example, there are different types of annuities, each entailing unique features, risks, and expenses. Be sure to talk to a tax or financial advisor about your particular situation and the options that may be best for you.

In addition to required minimum distributions, removing money from an employer-sponsored retirement plan involves some other issues that need to be explored. Often, this may require the assistance of a tax or financial professional, who can evaluate the options available to you and analyze the tax consequences of various distribution options.

Lump-Sum Distributions

Retirees usually have the option of removing their retirement plan assets in one lump sum. Certain lump sums qualify for preferential tax treatment. To qualify, the payment of funds must meet requirements defined by the IRS:

• The entire amount of your balance in an employer-sponsored retirement plan must be paid in a single tax year.

• The amount must be paid after you turn 59½ or separate from service.

• You must have participated in the plan for five tax years.

A lump-sum distribution may qualify for preferential tax treatment if you were born before January 2, 1936. For instance, if you were born before January 2, 1936, you may qualify for 10-year forward income averaging on your lump-sum distribution, based on 1986 tax rates. With this option, the tax is calculated assuming the account balance is paid out in equal amounts over 10 years and taxed at the single taxpayer's rate. In addition, you may qualify for special 20% capital gains treatment on the pre-1974 portion of your lump sum.

If you qualify for forward income averaging, you may want to figure your tax liability with and without averaging to see which method will save you more. Keep in mind that the amounts received as distributions are generally taxed as ordinary income.

To the extent 10-year forward income averaging is available, the IRS also will give you a break (minimum distribution allowance) if your lump sum is less than $70,000. In such cases, taxes will only be due on a portion of the lump-sum distribution.

If you roll over all or part of an account into an IRA, you will not be able to elect forward income averaging on the distribution. Also, the rollover will not count as a distribution in meeting required minimum distribution amounts.

Periodic Distributions

If you choose to receive periodic payments that will extend past the year your turn age 70½, the amount must be at least as much as your required minimum distribution, to avoid penalties.

This table shows required minimum distribution periods for tax-deferred accounts for unmarried owners, married owners whose spouses are not more than 10 years younger than the account owner, and married owners whose spouses are not the sole beneficiaries of their accounts.

Source: IRS Publication 590.

Other Considerations

If your plan's beneficiary is not your spouse, keep in mind that the IRS will limit the recognized age gap between you and a younger nonspousal beneficiary to 10 years for the purposes of calculating required minimum distributions during your lifetime.

Conclusion

There are several considerations to make regarding your retirement plan distributions, and the changing laws and numerous exceptions do not make the decision any easier. It is important to consult competent financial advisors to determine which option is best for your personal situation.