Higher Learning

During these uncertain times, 529 plans may make more sense than ever.

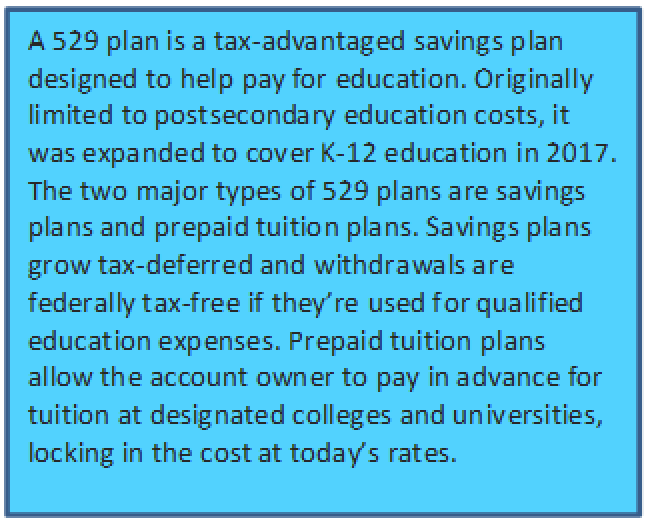

For many people, a 529 savings plan offers an opportunity to achieve an important life goal and improve overall financial health. As college and university administrators determine how higher education will look in the future (classes on campus, remote learning or a mix of both), the benefits of a 529 plan have never been more meaningful. Here are three benefits that are particularly important during these times — especially as the cost of higher learning continues to rise.

- Not only can 529 plan assets be used to pay for tuition and books, they can also pay for computers, internet access and other equipment. This will be especially important if remote learning continues indefinitely.

The recently passed Setting Every Community Up for Retirement Enhancement (SECURE) Act expanded qualified expenses to include registered apprenticeship programs1 and repayment of college debt.

- Account owners have full control over 529 plan assets and can even be the beneficiary of their own account. This is a huge benefit for anyone looking to go back to school right now to advance their skills for the evolving work environment and new opportunities that may come with it.

Follow the money

Distributions from a 529 plan can be used to cover a long list of qualified education expenses at qualified institutions. Here’s a summary:

Qualified expenses

K-12

• Tuition up to $10,000 per year per student

Postsecondary

• Tuition and fees

• Books, supplies and equipment required for enrollment or attendance

• Room and board (on- or off-campus for students who are at least half time)

• Computer peripheral equipment, software and internet access if used primarily by the beneficiary

• Special needs services as required by beneficiaries in connection with enrollment or attendance

• Fees, books, supplies and equipment required for participation in a registered apprenticeship program1

Types of eligible institutions

• In-state or out-of-state colleges

• Public and private schools

• Vocational schools

• Technical and trade schools

• International higher education institutions

• Any public, private or religious elementary or secondary school

• Registered apprenticeship programs1

• Repayment of principal/interest on any qualified education loan up to a $10,000 lifetime limit for the designated beneficiary