Everything's Better With Bacon

It even makes understanding inflation easier.

“Bacon’s the best. Even the frying of bacon sounds like applause. Bacon bits are like the fairy dust of the food community.”

– Jim Gaffigan

Let’s face it: talking about bacon is always fun. It can even help illustrate a topic that has been in the financial media a lot lately — inflation. In 1991, the price of a pound of bacon cost $2.22 (according to the Bureau of Labor Statistics). Thirty years later, in August of 2021, a pound cost $7.10. That’s inflation at work. Inflation is simply the rise in the cost of living, and it eats away at your money’s purchasing power and may not buy as much retirement in the future as it does today.

Over the past several months, inflation has crept back into the financial media limelight. Last year, price increases began to grow out of pandemic-related shutdowns and supply chain disruptions. As an example, the Consumer Price Index, a key measure of inflation, climbed 5.4% in September of 2021 compared with the prior year.

Keep Inflation in Mind in Your Retirement Planning

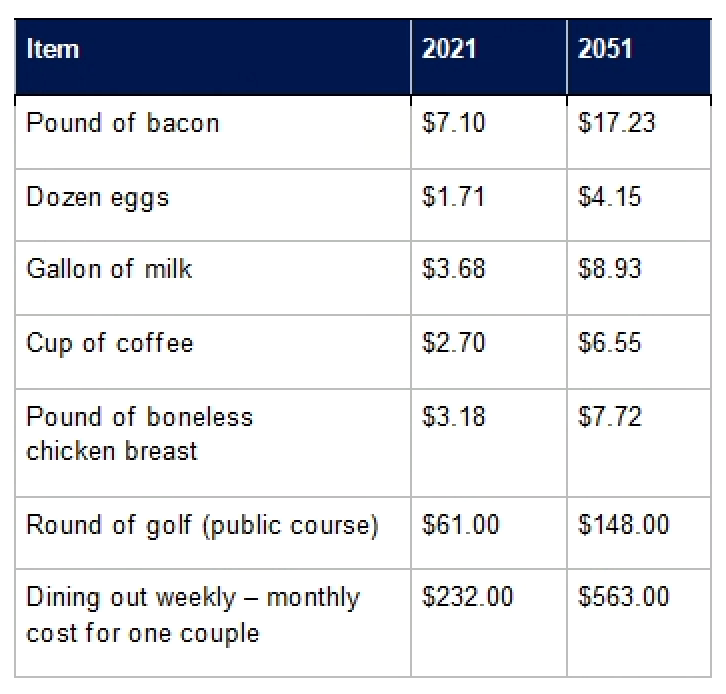

When you retire, one thing is a given: the cost of basic necessities as well as other things you enjoy will continue to rise. The following table provides some hypothetical examples to help increase your understanding of inflation.

2021 prices are based on Kmotion Research and general averages, including data from the U.S. Labor Department’s Bureau of Labor Statistics. Projections for 2051 prices assume a 3% annual inflation rate.

Get Real with Inflation

When managing inflation risk with your investments, it’s important to understand a couple of basic terms. Your nominal rate of return is the amount of money you make on an investment before expenses — this rate of return does not take inflation into account. Your real rate of return is the nominal return on your investment minus the inflation rate and gives you a better sense of the purchasing power of the money you make from your investments. For example, if your investment portfolio earns an 8% rate of return in a particular year, and the inflation rate is currently 3%, your real rate of return is just 5%.

Conventional wisdom says you should consider keeping an appropriate amount of your assets allocated to stocks and stock mutual funds to help offset inflation risk. Although past performance is no guarantee of future results, historical average stock returns have stayed ahead of inflation over the long term.